Home Mortgage Tips That Can Save You A Bundle

Content author-Guldborg FrandsenWhat sort of information does one need when considering a mortgage? Where can they find the best, most accurate, expert advice? This article has it all for you, from tips to help you engage in the process to tricks to help you get more out of your mortgage, so read on.

Always be open and honest with your lender. You don't want to just give up if you fall behind on your mortgage payments. If you talk with the lender, you can often find a workable solution benficial to both of you. Contact your lender and inquire about any options you might have.

Try not to borrow the most you can borrow. What you qualify for is not necessarily the amount you can afford. Know what you can comfortably afford.

Try to have a down payment of at least 20 percent of the sales price. In addition to lowering your interest rate, you will also avoid pmi or private mortgage insurance premiums. This insurance protects the lender should you default on the loan. Premiums are added to your monthly payment.

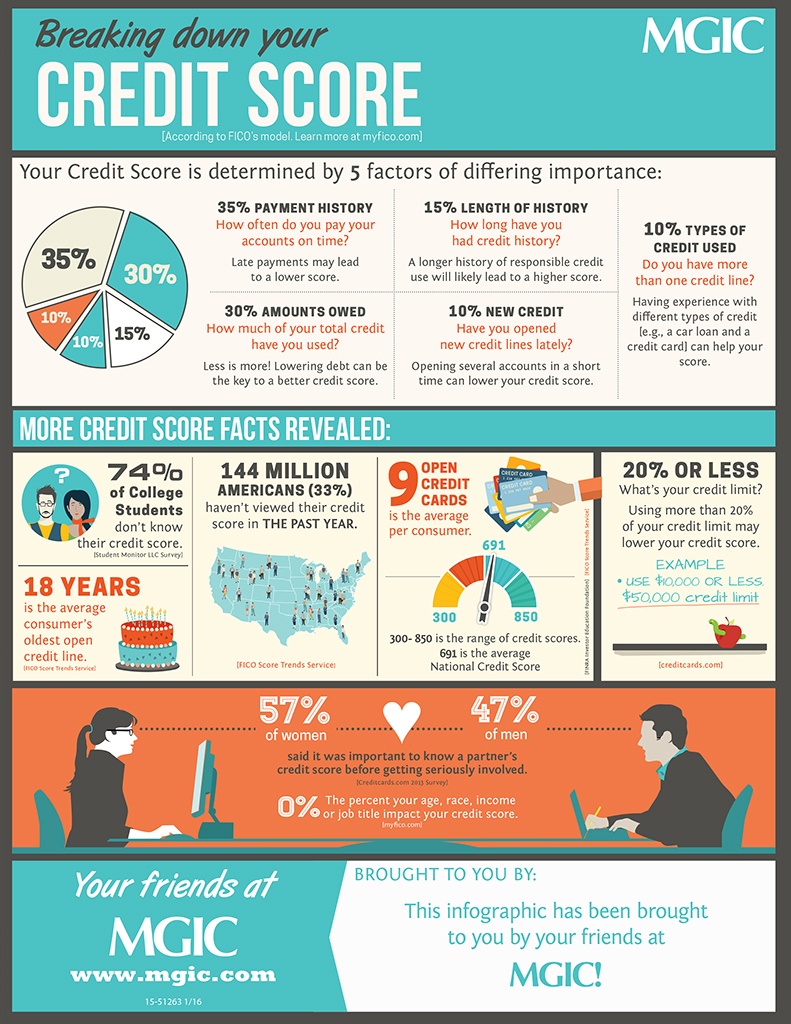

Don't make any sudden moves with your credit during your mortgage process. If your mortgage is approved, your credit needs to stay put until closing. After a lender pulls up your credit and says you're approved, that doesn't mean it's a done deal. Many lenders will pull your credit again just before the loan closes. Avoid doing anything that could impact your credit. Don't close accounts or apply for new credit lines. Be sure to pay your bills on time and don't finance new cars.

If your appraisal isn't enough, try again. If the one your lender receives is not enough to back your mortgage loan, and you think they're mistaken, you can try another lender. You cannot order another appraisal or pick the appraiser the lender uses, however, you may dispute the first one or go to a different lender. While the appraisal value of the home shouldn't vary drastically too much between different appraisers, it can. If you think the first appraiser is incorrect, try another lender with, hopefully, a better appraiser.

Look into no closing cost options. If closing costs are concerning you, there are many offers out there where those costs are taken care of by the lender. simply click the up coming site in your interest rate to make up for the difference. This can help you if immediate cash is an issue.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Keep in mind that not all mortgage lending companies have the same rules for approving mortgages and don't be discouraged if you are turned down by the first one you try. Ask for an explanation of why you were denied the mortgage and fix the problem if you can. It may also be that you just need to find a different mortgage company.

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

Learn about the three main types of home mortgage options. The three choices are a balloon mortgage, a fixed-rate mortgage, and an adjustable-rate mortgage (ARM). Each of these types of mortgages has different terms and you want to know this information before you make a decision about what is right for you.

Remember that there are always closing costs and a down payment associated with a home mortgage. Closing costs could be about three or four percent of the price of the home you select. Be sure to establish a savings account and fund it well so that you will be able to cover your down payment and closing costs comfortably.

Make sure you have done a little research on your chosen financier before you sign anything with them. Unfortunately, you can not always trust the spoken word. Ask friends and neighbors. Check online, as well. Research the entity with the BBB. Save thousand of dollars by arming yourself with the right information before you negotiate your loan.

Most financial institutions want the assurance that the property they finance is insured and the property taxes are current. They do this by requiring that you add an amount to cover those expenses to your mortgage payments. This is called an escrow account, and most people find it is convenient to set up payments this way.

Rebuild or repair your credit before shopping for a home mortgage. A good credit history and credit score qualifies you for a better interest rate. It is also frustrating to find the perfect house but not qualify for the loan you need. Taking the time to fix your credit before buying a house will save you money in the long run.

If you think you are able to afford higher payments, consider getting a 15 or 20 year loan. These shorter-term loans have a lower interest rate and a slightly higher monthly payment for the shorter loan period. In the long run, you can save thousands over a 30-year loan.

Reduce your outstanding liabilities as much as possible before applying for a home mortgage loan. It is especially important to reduce credit card debt, but outstanding auto loans are less of a problem. If you have equity in another property, the financial institution will look at that in a positive light.

If your downpayment is less than 20% of the sales price of the home you want to buy, expect the mortgage lender to require mortgage insurance. This insurance protects the lender in the event that you can't pay your mortgage payments. Avoid mortgage insurance premiums by making a downpayment of at least 20%.

Be sure you are honest when you're applying for a loan. If you aren't truthful, you may be denied the loan you seek. Lenders will not have faith in you if you tell lies.

As was stated in the introductory paragraph of this article, the mortgage financing process is very complicated. It can seem indecipherable to a real estate novice. The key to financing a great mortgage that allows you to buy the home of your dreams is to educate yourself on the mortgage process. Study the mortgage tips and advice in this article very carefully.